Oriental Bank scam and auditing

Iftekhar Hossain

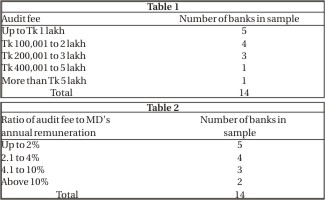

The Oriental Bank stench is continually increasing. As per the January 24 issue of The Daily Star it is now estimated to be Taka 595 crores. For those of us who are bank auditors and regulators, self-criticism is required on what role we play in prevention and detection of such frauds. The goal should be to create an environment where potential fraudsters think twice before embarking on the road to amassing quick money overnight, and to quickly catch them and send to jail. Bangladesh Bank, the regulator of the banking sector, is to be commended for detection of the Oriental Bank fraud. Now it is up to the regulator, and indeed the society, to mete out quickly exemplary punishment to the perpetrators. The bigger challenge, however, is to repair the hole in the environment which allowed such massive fraud. Was it fully due to the political corruption, or are there also weaknesses in the control environment? Statutory bank auditors are appointed by the shareholders in the Annual General Meeting (AGM). The audit is conducted by chartered accounting firms as per Bangladesh Standards on Auditing (BSA). These standards are adopted from the International Standards on Auditing (ISA). How many of the bank auditors have really gone through BSA 240: The auditor's responsibility to consider fraud and error in an audit of financial statements? We quote it to protect ourselves when allegations are made against us that we are not being able to detect fraud. However, do we ask ourselves whether we are complying with its requirements? When we start a bank audit do we comply with BSA 240.20: "In planning the audit, the auditor should discuss with other members of the audit team the susceptibility of the entity to material misstatements in the financial statements resulting from fraud or error." Again, BSA 240.22 requires the auditor to make inquiries of the management to obtain an understanding of: "(i) Management's assessment of the risk that the financial statements may be materially misstated as a result of fraud; and (ii) the accounting and internal control system management has put in place to address such risk." Do we send adequately trained people who can discuss these issues with management, or do we send personnel who do not have either the courage to talk with the managing director/board or the technical capacity? The general defence put forward by some independent bank auditors is that the extremely low audit fees do not allow him to comply with the requirements of BSA 220: Quality Control for Audit Work. The ICAB Fee Schedule of July 2004 states a minimum fee of Tk 250,000 for banks, increasing with the total assets or total turnover amount of the bank. The extremely low audit fee is a fact as shown in Table 1 on some sample private commercial banks as per their audited accounts for year 2005 published in the newspapers. 10 of the 14 banks (71%) were audited below the minimum fee of the ICAB schedule. A comparison was made between the audit fee and the managing director's annual remuneration. As shown in Table 2 there is considerable variation between what the bank's pay to its chief executive and what is paid to the watchdog. Some managing director/board's try to justify the low audit fee by saying that they have no control on the audit fee which is approved in the AGM by the shareholders. The fact, however, is that in most cases the board controls a majority share of the votes, and it may be to their advantage not to have a quality audit. In view of the Oriental Bank fraud, it is high time that the banking regulator and the regulator of the independent audit profession (The Institute of Chartered Accountants of Bangladesh) look closely at this issue of statutory bank audit quality and bank audit cost. The author is a partner of ACNABIN, Chartered Accountants.

|