Taking stock

Mamun Rashid

Whatever the positive vive going around after the new interim government took over, 2007 continues to prove to be an unpredictable year for Bangladesh and the recent performance of the country's stock market mirrors that unpredictability. Over the last ten to twelve business days, the daily traded volumes on the country's bourses have not only surpassed their 1996 highs but making news every day by beating the prior day's record volume currently averaging between $12-$15 MM and reaching as high as $25 MM per day versus last year's average of approximately $5 MM everyday. As stakeholders watch this interesting phenomenon of the trading volumes in the market reach dizzying levels, here are some points to ponder: Investor sentiments: Judging by the comparatively modest gains of the overall market capitalization of around 8% in 2007 YTD and a healthy but balanced visible primary issuance pipeline for the year compared to the surge of almost 300% in trading volume, the investor community seems to have developed a 50:50 split regarding the future direction of the market. There is a distinct divergence in investor expectations of the future with as many sellers as there are buyers with opposing expectations thus keeping prices at existing levels. What then is driving this trading frenzy among investors? Who are the net buyers and who are the net sellers? Are they different investor types? If political stability and positive economic outlook are truly the main drivers, why isn't it being reflected in the market capitalization going up concurrently? Do investors gain in the short run when there is higher market liquidity? Role of the market intermediaries: The market intermediaries make money when the investors sell and they make money when the investors buy. Higher trading volume translates into higher brokerage economics. In a traditionally retail driven market with minimal disciplined institutional research, what role are the financial intermediaries playing in promoting this sudden liquidity in the market? As the biggest gainers from the recent market activities, how unbiased are they from promoting market manipulation?

Surveillance: The stock market surveillance mechanics of 2006 has no resemblance to that of 1996. There are strict rules and guidelines and trading circuit breakers and international surveillance teams and the whole nine yards to protect investor rights and ensure fair play. The current phenomenon requires careful monitoring of investor motivation, monitoring of the role of the intermediaries in being able to effectively facilitate trade and most importantly monitoring of the financial and operational readiness of all the stakeholders should this trading volume surge be followed by a surge in the overall market capitalization. As market liquidity swells and tests news levels, can the regulatory mechanics keep up?

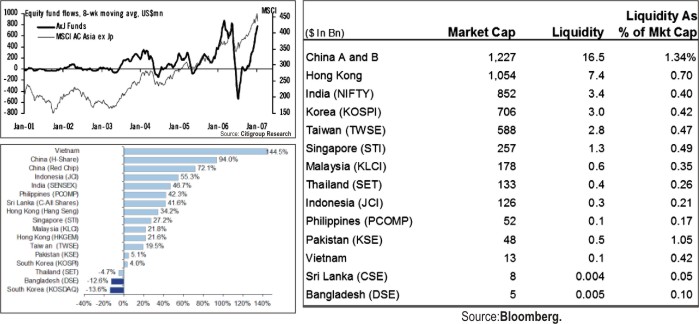

What's going on around the Region? Trading volume and liquidity continue to experience unusual highs across the region in all Asian markets on optimism of exceptional corporate earnings. Global equity markets recorded new multi-year highs in 2006 after a brief summer lull, with the Asia Pacific regional markets leading the pack. On average, Asian markets were up 32% during the year. China H-shares and Red Chips, Indonesia and India outperformed the region with large market capitalized names in the energy, FIG and consumer sectors contributing the most to the performance during the year. Some of the key market drivers for the Asian markets include:

Liquidity conditions: Liquidity tightened during the summer of 2006 but had regained momentum toward the end of the year and continue to do so.

Foreign fund inflows: Overwhelming response for Asian equity from global funds underscored demand in the region. In 2006, net inflow into Asian dedicated equity funds was at a record of US$16.8 Bn. Citigroup research expects the strong inflows to continue into the early part of 2007 after which, investors will be more selective.

Equity supply-demand: Heavy primary issuance supply of $80 +Bn from Asia Pacific region ex-Japan specifically from China and the financial institutions sector were well absorbed in 2006 with strong sustained aftermarket performance. 2007 is expected to see regional Asia Pacific primary issuance of an equal amount. On the other hand, Bangladesh equities ended the year down 12.6% in 2006 driven by investor skittishness related to political uncertainty; export disruption and expectation of a slowdown of domestic consumption, despite a record GDP growth of 6.7% and strong macro micro fundamentals. Are Bangladeshi equities with a growing liquidity to market capitalization ratio now ranging around 0.3-0.5% from last year's 0.1% now playing long overdue catch-up with the rest of the region or this the current buoyancy a temporary market anomaly/blip?

Next steps for BangladeshWhat could help sustain the current positive investor sentiment and translate the increased liquidity to actual increase in overall market capitalization in the country's bourses? The timing may be right for Bangladesh to come out of the vicious Catch 22 situation of lack of issuers due to lack of investors and lack of investors due to lack of issuers.

Without seeming to know it all and without a crystal ball to predict next steps, we outline below some suggestions for the stakeholders to help carry on the current momentum and create a sustainable public equity market and attract investors and corporate issuers alike to play:

Issuers

Incentivize good issuers with proper financial and corporate governance disclosure and transparency to access capital markets as a viable and sustainable source of capital.

* Continuity in incentives from listed status: Provide comfort that existing tax incentives for issuers will not be subject to change with a change of guard at the government offices.

* IPO proceed maximization: Introduce book-building as soon as viable to allow play of demand and supply in the market to determine issue price and allow for issuers to maximize proceeds.

* Incentivize government SOEs to access capital markets: The subcontinent has recently seen a proliferation of state owned entities privatizing via sale of shares to international equity investor which serves as a sizeable and attractive investment proposition to draw foreign equity capital inflow into the country.

* Institutional investor participation: Facilitate participation from responsible institutional investors to own substantial shares in companies through the use of pre-IPO placements thus also ensuring responsible aftermarket trading.

* Regulatory support: Ensure on-going regulatory support for listed issuers without undue penalty/scrutiny. Investors Incentivize responsible long-term institutional investors to play in the local capital markets to add market depth and discipline. Liquidity is not a problem in this current global equity market.

* Ensure strong investment opportunity pipeline: Attract domestic and foreign investors to the capital markets via development of healthy pipeline of primary issuances and strong aftermarket support. Foreign investors seek sizeable investment opportunities upward of $5 MM or so in one order size to make their involvement cost effective and would shy away from the local markets if the right opportunities didn't present themselves regularly in sizeable amounts.

* Active marketing to right investor community: Actively market Bangladesh equities, the country's private sector growth potential and the change in regulatory environment post 1996 among responsible long-term foreign institutional investors and NRBs through use of international conferences, road shows and other formal marketing efforts. Strong opportunity for Bangladesh to leverage bullish sentiment among regional investors to attract foreign capital inflow. The $30 MM of recent inflow serves as good indication of the excess capital globally seeking good returns. If the Bangladesh of 1996 could have attracted $100 MM of equity and if Vietnam has excess of 15 country funds, then tremendous potential for massive capital inflow into the country's bourses with the right marketing efforts. In addition, active marketing and promotion of Bangladesh as a frontier economy (Vietnam, Zimbabwe) versus an emerging economy (India, Korea, China) could further facilitate additional attention and capital allocation from the Frontier Funds.

* Benchmarking: Facilitate valuation of the investment opportunities through creation of benchmarks at the country level. A sovereign rating of the country from the internationally accepted rating agencies would enable institutional investors to effectively evaluate sovereign risk and make investment decisions.

* Reliable regulatory environment: Build investor friendly regulatory framework to ensure fair market plays and discipline in trading. Create precedence of fair support from regulators in an investor dispute.

* Protect retail investors: Protect the interests and capital of the retail investor base through regulatory supervision and formalized investor education on investment risks. Intermediaries Incentivize responsible long-term local and foreign intermediaries to participate in the markets as advisors of investors and issuers.

* Proper economic incentive: Allow fee structure (IPO, brokerage) to be negotiated between the institutional stakeholders without excessive regulatory restrictions such that there is proper economic incentive for professionals to enter and play in capital markets.

* Fiduciary responsibility: Create environment of fiduciary responsibility for all intermediaries to minimize market manipulation. Whatever said and done, Bangladesh remains to be a potential country with possible future. Provided we are aware of our destination model and work towards paving the way for growth for all of us, with ultimate transparency, proper knowledge and commitment to the future of the nation. Mamun Rashid is a banker and nominated director of Chittagong Stock Exchange.

|