Inside

|

Revenue Growth during FY08: No room for complacency Zaid Bakht and Md. Nazmul Hoque dissects the latest economic figures

The latest available official data shows that the National Board of Revenue (NBR) collected Tk 31,046 crore as tax revenue during July-March of the current fiscal year. This figure is nearly 23.1% higher than the revenue collected by the NBR over the corresponding period of the preceding year. Given that the target growth in NBR tax revenue for the overall year has been set at 17% in the national budget for FY08, NBR's tax revenue earning during the first eight

months has surely been commendable. During 2006-07, NBR tax revenue accounted for 95% of total tax revenue and 80% of all revenue collected. The observed growth in NBR tax revenue, therefore, may be considered as reflective of the buoyant overall revenue earning in the economy during the current fiscal. At the disaggregate level, the highest growth in this year's revenue earning has been recorded in the case of income tax (35.6%), followed by indirect tax (VAT, SD, ED) from domestic

sources (22.45%) and indirect tax (Custom duty, VAT and SD) from import sources (17.68%). Major policy measures that seem to have contributed to this revenue performance include: (a) the on-going anti-corruption drive of the caretaker government, (b) the scope of regularising undeclared income by paying penalty taxes, (c) the provision of universal self-assessment return for payments of income tax, and (d) raising of custom duty on the import of capital machinery, raw materials and intermediate goods.. One, however, needs to apply at least two qualifications to the above mentioned optimistic scenario with regard to revenue growth. First, FY07 was a low performing year as the rate of growth of NBR tax revenue earning in that year was only 9.3% against 13.6% in FY06 and 14.2% in FY05. Therefore, growth rate for FY08 has been calculated against a relatively low base and hence appears larger. Second, and more importantly, both import and domestic prices have experienced significantly higher rates of increases in the current year than the previous year and, therefore, the observed growth in NBR tax revenue is likely to be more in nominal than in real terms. Higher prices of goods and services imply higher collection of VAT, supplementary duty, and import duty for the same volume of goods and services transacted.

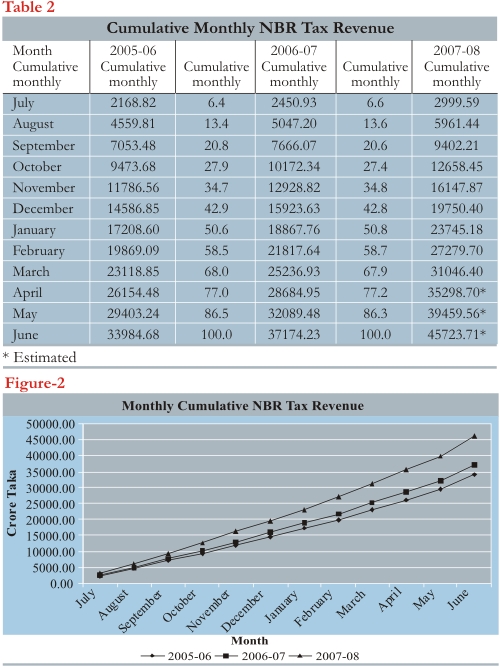

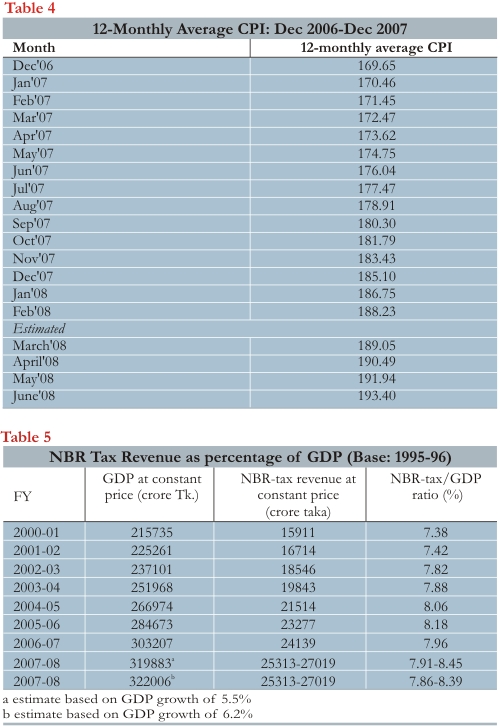

To examine these issues, we estimated yearly NBR tax revenue at constant 1995-96 prices for the period 2000-01 to 2006-07 by deflating the revenue series at current price with the GDP deflator and fitted linear trend lines to both nominal and real series. The relevant data have been presented in Table 1 and the trend lines have been shown in Figure 1. We then tried to estimate nominal NBR tax revenue earning for the whole of FY08 based on the data for the first nine months of the year. For this purpose, we looked at the monthly figures of NBR tax revenue for FY06, FY07 and FY08. The relevant data have been presented in Table 2 and the picture has been depicted in Figure 2. Based on the observed regularity of the monthly trends, we have estimated cumulative NBR tax revenue for the remaining four months of the current fiscal year. This gave us an estimated NBR tax revenue of Tk 45,724 crore for FY08. To convert the estimated nominal yearly revenue figure to constant 1995-96 value, we need an estimate of the GDP deflator for FY08. For this purpose, we compared the movement of CPI with the movement of the GDP deflator during the period 2000-01 to 2006-07 (Table 3). As can be seen from the Table, the ratio of GDP deflator to CPI varied from a low of 0.875 to a high of 0.934 in recent years. For the current fiscal year, CPI data is available for the first eight months only. Table 4 and Figure 3 show 12-monthly average CPI for the months Dec'06 to Feb'08. We fitted a semi-log function to this data (Adjusted R2=0.99) and on the basis of the regression parameters, estimated 12-monthly average CPI for the remaining four months of the year. As can be seen from the Table, the estimated average annual CPI for FY08 is 193.40. Using this CPI we derived two estimates of the GDP deflator based on the low and the high GDP deflator/CPI ratio. The estimated GDP deflators are 169.23 and 180.64 respectively. Using these deflators, NBR tax revenue for FY08 at constant 1995-96 is estimated to be Tk 27,019.48 crore and Tk 25,312.68 crore respectively. In contrast, the trend value of NBR tax revenue for FY08 in constant price is estimated on the basis of the trend line fitted in Figure 1 to be Tk 25,818 crore. Our estimate of revenue earnings at constant price based on low GDP deflator/CPI ratio is only 4.65 per cent above this trend value while the estimate based on higher GDP deflator/CPI ratio is about 2 per cent less than the trend value.

There are several reasons why current year's GDP deflator is likely to bear close correspondence with the CPI: The implication of this is that the GDP deflator/CPI ratio is likely to be on the high side and therefore, despite impressive growth in revenue earning in nominal terms, estimated yearly revenue earning in constant price is likely to fall short of the trend value. In the event of a low GDP deflator/CPI ratio, the yearly revenue earnings at constant price is expected to exceed the trend value but only by a modest margin.

A similar picture emerges when one looks at the NBR-tax/GDP ratio. Table 5 presents the relevant ratio for the period 2001/02 - 2006/07. As can be seen from the Table, the NBR-tax/GDP ratio hovered around 8% during this period. For 2007-08, we projected GDP at constant price based on a low rate of GDP growth of 5.5% and a high rate of GDP growth of 6.2%. Given our alternative estimates of NBR tax revenue for 2007-08 at constant price, the NBR-tax/GDP ratio for 2007-08 is seen to vary from a low of 7.86% to a high of 8.45%. This suggests that the tax/GDP ratio is unlikely to be significantly high during the current year despite high growth in revenue earnings in nominal terms. It may be mentioned here that the PRSP target of tax/GDP ratio for 2007-08 was set at 9.6%, which implies a NBR-tax/GDP ratio of approximately 9.12% given the share of NBR-tax in total tax revenue. Our estimate of NBR-tax/GDP ratio for 2007-08 clearly falls way below this target. The observed growth of revenue earnings in nominal terms has been interpreted by some quarters as the sign of vibrancy of the economy contesting the view that Bangladesh economy experienced any major slowing down during the current fiscal year. The evidence presented clearly contradicts that notion. It shows that the success achieved in revenue earning due to anti-corruption drive could hardly make up for the loss in revenue earning due to slowing down of the real economy.

If the economy had sustained the growth momentum it achieved in the earlier years, revenue earnings would have significantly exceeded the trend value given the higher motivation for tax payment induced by the anti-corruption drive. Again, our estimate of the yearly revenue earning is based on the expectation that this motivation will be sustained till the year-end. If that falters for any reason the picture may get even less optimistic. There is thus, hardly any room to be complacent about the current revenue earning situation. Zaid Bakht is Research Director, BIDS, and Md. Nazmul Hoque is Research Associate, BIDS.

|