Inside

|

How Will the Global Economic Slowdown Effect Bangladesh? Jyoti Rahman points out the grim economic possibilities that we should all be aware of

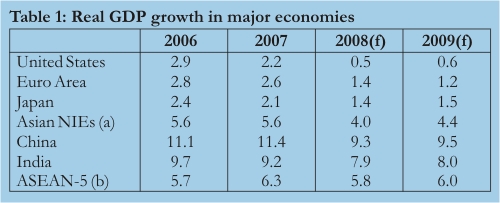

These are difficult times for the global economy. Economic growth is weakening around the world, reflecting the fallout from the sub-prime mortgage crisis and associated financial market turbulence. A recession appears to be imminent in the United States -- the question now is about its severity and length. Other developed economies are also expected to slow. As are, to a lesser extent, major emerging economies in Asia. And the slowdown is happening in a period of significant inflationary pressure, complicating the job of macroeconomic policymakers. What has caused the slowdown? What is the global economic outlook? What is the outlook for Bangladesh? If the global slowdown is much more protracted than the current forecasts, what would be the impacts on Bangladesh? I try to explore these questions in what follows. I also touch on some difficult macroeconomic policy choices facing our policymakers. Global economic outlook Table 1 shows the IMF's latest economic growth forecasts for the major economies.

The proximate cause of the US recession is its housing sector. Construction of new houses has fallen sharply, reflecting an unwinding of an oversupply of houses. Exacerbating the construction downturn are rising mortgage default rates -- particularly the sub-prime ones -- and falling house prices. Flowing on from all this is an intensifying credit squeeze -- put simply, banks and lending institutions have become extremely cautious, denying loans to some borrowers who have projects that would have been funded in other, less turbulent, times. The housing and financial market developments are mutually reinforcing. As a result, the IMF's baseline scenario has the US economy dipping into a mild recession in 2008. The US accounts for a quarter of the global economy, and has important trade and financial linkages with every economy around the world. Historically, US recessions have caused slowdowns in other major economies. Hence the adage: when the US sneezes, the world catches cold. That's why the IMF forecasts sluggish economic growth projections for the other developed economies. The IMF does not, however, forecast quite as dramatic a slowing in the emerging Asian economies as it does for the developed world. This is broadly consistent with the "decoupling hypothesis," which holds that major Asian emerging economies -- China and India, but also the smaller ones such as the NIEs or the ASEAN-5 -- have matured enough so that the US recession might not affect them as much as was the case in the past. In its latest Asian Development Outlook (ADO), published in March, the Asian Development Bank examines the decoupling hypothesis using a number of techniques. The ADB concludes thus: Developing Asia is not immune to global developments, but neither is it hostage to them. Citing structural transformations, robust productivity growth, and favourable policy climate, the ADB forecasts that the Asian economies will experience a moderation in growth, rather than a sharp downturn.

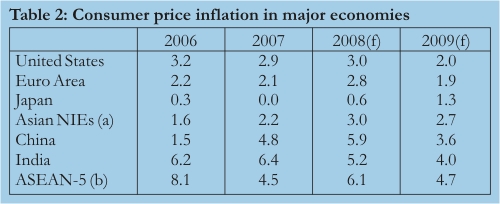

The IMF also forecasts inflationary pressures to continue in both the developed and developing worlds (Table 2). There are two reasons for the recent rise in inflation around the world. Firstly, the robust growth of the developing world -- particularly the large economies of India and China -- has been causing rapid rises in demand for food and energy commodities. With supply lagging demand, their prices have risen to record highs. With growth expected to continue in the emerging Asian economies, the prospect for commodity prices are still high. Subsidies to bio-fuels are the other major reason for the recent rise in global food price inflation.1 These subsidies are politically popular, and it is unlikely that they will be removed, particularly in an election year in the US. The inflationary environment makes the macro-economic policy-makers' job -- the restoration of stability in housing and financial markets without setting off a spiral of inflationary expectations -- in the US and other affected economies all the more challenging. Plus, history gives grounds for pessimism. The last time the world economy experienced inflationary shocks generated by a commodity boom was in the 1970s. It ended in a period of high inflation coupled with high unemployment and sluggish growth, an episode dubbed as stagflation. And recessions that involve major damages to the financial systems and housing markets tend to last much longer than other recessions, with the Great Depression of the 1930s being the most extreme example of how bad things could get. On the plus side, the Federal Reserve Chairman Ben Bernanke -- who spent much of his stellar academic career studying the Great Depression -- appears to have the confidence of the market, and neither a depression nor a stagflation is on anyone's baseline scenario, yet. Economic outlook for Bangladesh

According to the ADB, the slowdown in economic growth in the 2008 financial year "is attributed to the erosion of business confidence and the effects of the natural disasters." The projected recovery in 2009 rests on the assumptions that business confidence will return and there will be "substantial external assistance" to mitigate the effects of the natural disasters. Looking into the sectoral components of GDP, the economic slowdown is most evident in the industry sector. Growth in production and exports of garments and knitwear has been much weaker in the current financial year. In addition to business confidence, a combination of other factors has been responsible: labour turmoil in the previous years; very weak demand from the US; and higher raw material import costs. A sharper than expected US recession and continued price rises in the global market are of course likely to dampen industrial production and export growth even if business confidence were to be restored. Agriculture has been hurt by the natural disasters, and its recovery is to a large extent at nature's mercy. In contrast, the service sector is expected to experience a much more modest slowdown, as strong remittance flows are expected to continue to shore of up consumption. The ADB expects inflation to remain high throughout the forecast period. Higher inflation is attributed to: rising commodity prices -- particularly foodgrains and oil -- in the global market; the domestic foodgrain shortfall; and the lagged effect of higher than programmed monetary expansion. In addition to the perennial threats of political upheaval and natural disasters, rapidly growing inflation is listed as a major near-term risk to the outlook. The ADB warns: the failure to rein it [inflation] in could seriously undermine political and economic stability. Implications for Bangladesh of a worse-than-expected global slowdown There are three major channels through which a worse-than-expected global slowdown could affect Bangladesh: investment, exports, and remittances. Let's consider investment first. Should the credit squeeze worsen in the global financial markets, interest rates are going rise even more. Further, at times like this, there is a "flight to quality" -- that is, lenders seek the relatively less risky borrowers. As a result, credit spreads will widen, and Bangladeshi businesses will find it harder to borrow. This, in turn, will hurt investment. The flight to quality will also mean foreign direct investment might dry up. In the near term, sharp slowdown in investment will hurt employment and household income, with flow on effects on consumption. In the medium term, slowdown in investment, particularly foreign direct investment, will hurt industrialisation, technology transfer, and productivity growth -- all very important factors for poverty alleviation through sustained economic growth. The second channel through which a worse-than-expected slowdown could affect Bangladesh is exports. About a quarter of Bangladesh's exports are to the US, with Germany, the United Kingdom, France, and Italy accounting for another third. If the US recession is worse than anticipated, or if one or more of the major European countries enter a recession, exports will suffer. A sharp slowdown in exports will have additional impacts on investment, employment, and household income. Remittances will also suffer, especially if the credit squeeze worsens. This is because most non-resident Bangladeshis, particularly those living in the developed economies, will have to pay higher interest payments in their house mortgage, credit card debt, or personal loans. Remittances have shored up household income and boosted consumption in recent years. If remittances were to start drying up, consumption will hurt, and the service sectors such as financial services, property, and telecommunications will suffer. Macro-economic policy options Some possible policies -- food for work programs, greater government investment in rural infrastructure projects to generate rural employment -- are worthwhile in their own right, regardless of the inflation situation. However, to the extent that they cost money, their implementation is problematic, as the government's coffers are already in the red. The ADB forecasts a budget deficit of 4.8 per cent of GDP in the 2008 financial year. The Economist puts the number at 5 per cent. Unless the food subsidies and related programs were financed by external assistance, the government will have to make some difficult choices. Other policy options -- liberalisation of foreign investment regimes to encourage new energy projects, or policies aimed at improving agricultural productivity -- may not require much government expenditure, but will not yield results immediately. And in an environment of 40 taka per kg of rice, calls for subsidies that assist the poor here and now will be very difficult to ignore for the government. If significant external assistance is not forthcoming, the government will have to either cut expenditure elsewhere and/or raise taxes, or finance the widening deficit somehow. The former option presents obvious political difficulties. The latter presents significant macro-economic risks. In an already tight global credit market, government borrowing to finance widening budget deficit will crowd out private investment. Alternatively, if the Bangladesh Bank were to finance the deficit by printing money, we would be taking the first steps to hyper-inflation. Even the most optimistic scenario -- one of a very mild US recession and a quick global recovery -- still leaves our macro-economic policymakers with little wiggle room. As long as inflation remains high, our policymakers will have to balance difficult policy trade offs. If the worst should happen -- a protracted global slowdown with continued inflation -- we could be looking at the worst economic crisis since the 1970s. This is indeed a very bleak outlook, with no good policy options. It is in this environment that the budget will be brought down. And quite possibly, the newly elected government will inherit a more challenging set of tasks than any of its predecessors in decades. No matter what happens in the political arena, it is important that this grim situation is understood. 1. See here: http://www.thedailystar. net/forum/2008/February /food.htm Jyoti Rahman is an applied macroeconomist and a member of Drishtipat Writers' Collective. He can be contacted at dpwriters@drishtipat.org.

|