Inside

|

Share the Wealth Ifty Islam argues that it's high time for new quality shares to enter our capital market

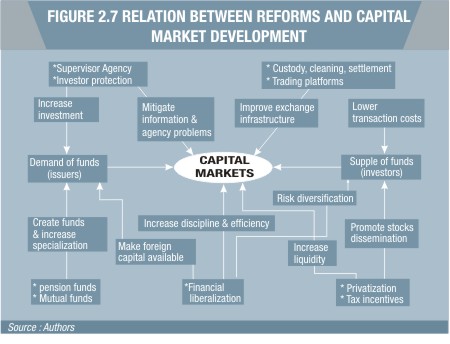

With the successful IPO of Grameenphone (GP), market capitalisation has risen to $32.9 billion (30 per cent of GDP) versus $3.2 billion and 6 per cent just 5 years ago. Turnover has increased by a factor of 30 times over the same period, averaging around $140 million daily. While foreign participation in the equity market remains low at around 1 per cent, this lack of effective integration into global financial markets was undoubtedly a blessing in disguise in shielding Bangladesh from the bulk of the spillover from the global financial crisis. However, there have been growing concerns from a number of capital markets observers that the Bangladesh stock market is becoming a "bubble." This might be defined either as a market where price levels are substantially in excess of fundamentally justified levels as a result of excess liquidity or potentially a speculative element whereby some investors are merely buying because prices are rising rather than by an assessment of fair value. Recently the finance minister has alluded to the "shallowness" of the market, whereby there is a growing demand/supply imbalance for stocks. In this article we will be primarily focusing on how to increase the supply of equities, and deal with the issue of excess demand in a future piece of analysis. A combination of weak investment demand for capital investment from the corporate sector and strong remittance inflows has left the banking system with excess liquidity of up to Tk 35,000 crore at its peak. This excess liquidity has manifested itself in asset price inflation in both equities and real estate markets. Clearly one solution to the supply/demand imbalance is for Bangladesh Bank to mop up excess liquidity through its money market operations. However, this should be done in conjunction with increasing the supply of new stocks coming to the market place. We will focus on measures to improve the supply side in the balance of this article. Corporate Financing Decisions in Developing Countries Broadly speaking, economies can be characterised as being either stock market-oriented or bank-oriented. Traditionally, the UK and U.S. economies have been regarded as being stock market-oriented while Japanese and German economies are regarded as being bank-oriented. In this framework, Bangladesh, like India and other countries in South Asia, can be considered a bank-oriented system. Drawing on some of the work from Marvin Goodfriend, professor of economics at Carnegie Mellon University, one can characterise the evolution of corporate financing needs and strategy, and implicitly the growth of capital markets in developing economies, as follows: In the earliest stages of economic development, firms finance investment by building up savings from internally generated funds. Self-funding is supplemented by loans from close relatives, extended family members, friends in the community and the like. Such "inside" funding overcomes information and credibility problems, and provides an incentive for owners to use the funds energetically, as promised. The borrower is bonded by its close relationship to family and community. Indeed, close relationships monitor the borrower's behaviour and can enforce discipline on the borrower if need be. As an economy develops, self-funding and inside funding become insufficient to finance firms that must manage complex production processes and serve broader markets. Firms must attract additional financing from external sources. Banks arise to provide information-intensive external funding, and, in effect, recreate the kind of information, bonding and monitoring that come with family relationship lending, only with more funding. The cost of external funding through banks involves credit evaluation, loan monitoring, and a component to allow for the risk of default and the cost of managing a default if it occurs. These costs of external finance create an external finance premium that a borrower must pay over and above the opportunity cost of self-funding or funding from close associates. Too much reliance on bank loans or direct bond finance, however, exposes a firm to excessive risk of bankruptcy in the event of default. Hence, in developed economies firms have come to rely on a portfolio of external finance that usually includes substantial equity, as well as bond and bank loan finance. Equity finance gives a firm financial flexibility in the choice of the payment of dividends -- flexibility that a firm can utilise to avoid default on bank loans or bonds. Outside equity, however, involves a cost of its own: too much of it blunts the incentive of managers to run a firm efficiently because external ownership allows managers to retain only a fraction of every dollar of value they create for the firm above revenue needed to pay off fixed obligations, which include debt and fixed salaries. Therefore, equity, bank loans, and bonds generally co-exist in the capital structure of modern corporate borrowers. At a more practical level, taxation would bias the financing choice towards debt if, for example, corporate income is taxed but interest payments are tax deductible. This is an important factor in developed economies but much less so in developing ones. A much more relevant issue in countries like Bangladesh and India is that in emerging markets with strong family ownership ties, the issue of control may play a larger role, causing firms to defer issuing equity to avoid diluting control. Agarwal and Mohtadi (2004) examine the financing choice of firms by focusing on the determinants of the debt-equity ratios of firms in 21 developing countries for a period of 18 years (1980-1997). They find that find that: The results show that stock market development as measured by market capitalisation is significantly and negatively associated with the firms' debt levels relative to their equity position, while banking sector variables (especially bank deposits) are significantly and positively associated with debt equity ratio. The issue around appropriate leverage in listed companies will become increasingly important, as has been the case in more developed markets, where analysts and investors have firm expectations on optimal sector and company capital structures. Listed companies with excessive leverage, and indeed companies not availing debt optimally, are often punished by the markets in developed economies with reduced valuations. As the Bangladesh capital market becomes more institutionalised with professional asset managers managing pools of capital, one will inevitably see a more systematic assessment of balance sheet risk and its impact on equity value.

Measures to Stimulate Increased Equity Issuance Fairer IPO pricing with the adoption of the book-building method: One ongoing concern preventing a number of companies from listing has been what they have perceived as an inequitable IPO pricing mechanism, with the substantial premium new issues traded on listing reflecting a low valuation assigned by the regulator. In a simplified sense, companies did not have an incentive beyond the tax we highlight below to sell themselves "cheaply" on the stock market. However, with the adoption of book-building, companies are likely to be incentivised to come to market Regulations and tax incentives for increased free float: The SEC and Ministry of Finance have come up with a series of minimum direct listing requirements. However, we would recommend that they consider amending the existing tax incentive of 10 per cent corporate tax differential for non-financial listed companies to a differentiated tax incentive that increases the benefits for those companies over a certain size with a greater free float in the market place. Accounting irregularities as a constraint on listing: A more challenging and controversial issue is that some companies that understate their earnings and assets to minimize their tax liability might be dissuaded from listing given that the valuation they would receive for their company would be significantly less than a "fair" value based on a true representation of their company accounts. While one might argue there should be no exemptions that would cause moral hazard on mis-reporting of accounts, it might be worth considering a tax amnesty where those companies that chose to restate their accounts as part of a listing process would avoid fines to restate their accounts. If the tax incentives for listing were significant enough then perhaps more companies would choose to restate. Development of a mechanism whereby companies can raise the capital they need and meet free float requirements: The current IPO (i.e. capital raising) listing rules and mechanism are distinct from the direct listing rules and mechanism (i.e. offloading of shares). In order to achieve benchmark free float requirements and raise the desired amount of capital, we would recommend that the mechanisms are combined whereby a company listing can both raise capital and sell shares at the same time and pricing. This would ensure that companies can raise the amount of capital they need and use the capital raised productively thus enhancing shareholder value, but also fulfill free float and stock liquidity requirements by selling shares into the market.

Increased listing of state-owned enterprises: There has been growing enthusiasm for accelerated listing of SOEs as a means of increasing supply on the stock market. While we believe there are merits in terms of economic efficiency as well as redressing the supply/demand imbalance in the capital markets, this is unlikely to be a short-term fix. The state banks are likely immediate candidates for listing, but the authorities need to be careful that the companies they wish to privatise have been restructured and are financially viable before coming to market. The listings of Titas Gas, PGCB, and Desco have been received with much enthusiasm; as such, this can be extended to state-owned power plants, utilities, airports, hotels, transportation companies, jute mills, paper mills, fertiliser factories, etc. Private equity investment: Again, not a short-term solution, but private equity investors are primarily interested in exiting their non-market investments, and the favoured method in a developing economy like Bangladesh would be an IPO. So the authorities should look to encourage both the growth of the domestic PE industry as well as attract international PE investors to take stakes in BD companies. Conclusions We remain confident that the high P/E ratio of the market as well as the ongoing frustration among corporates on high nominal bank lending rates will see a significant acceleration of IPOs in the next 12-18 months. More companies looking to globalise are feeling increasingly capital constrained and will likely come to market. Likewise, we believe that a significant amount of the estimated $35 billion of infrastructure financing needs of Bangladesh can come from the capital markets with the necessary institutional reforms. This positive outlook notwithstanding, in the near term the monetary authorities may need to address the excess liquidity in the market-place until the supply side can catch up. References: Ifty Islam is the founder and Managing Partner of AT Capital.

|